With so many prospective EV contenders, it can be difficult to gauge which companies will emerge successful over the next decade. For example, Lordstown Motors (OTCMKTS:RIDEQ) forecast production of 98,800 vehicles between 2021 and 2023 in its 2020 investor presentation. In reality, Lordstown produced only 31 vehicles for sale as of January and filed for bankruptcy just five months later.

Unrealistic forecasts and snazzy concept designs have been extremely successful in attracting retail investors. However, it takes more than made-up internal numbers and finely pressed steel to succeed in the competitive EV market.

Today, Tesla (NASDAQ:TSLA) is undoubtedly the EV leader. At the same time, some investors argue that its $800 billion market capitalization could limit its future returns when compared to its smaller competitors. That’s led to significant interest in companies such as Rivian (NASDAQ:RIVN), Lucid (NASDAQ:LCID), Mullen Automotive (NASDAQ:MULN), Nio (NYSE:NIO) and Nikola (NASDAQ:NKLA).

Picking a winning stock isn’t an easy task by any means. Still, there are several factors that can provide hints about a company’s future potential, such as revenue growth, profitability, margins, and competitive advantages. Let’s take a look at how these five EV stocks stack up.

EV Stocks: Revenue and Revenue Growth

{kind=link}

{kind=link}

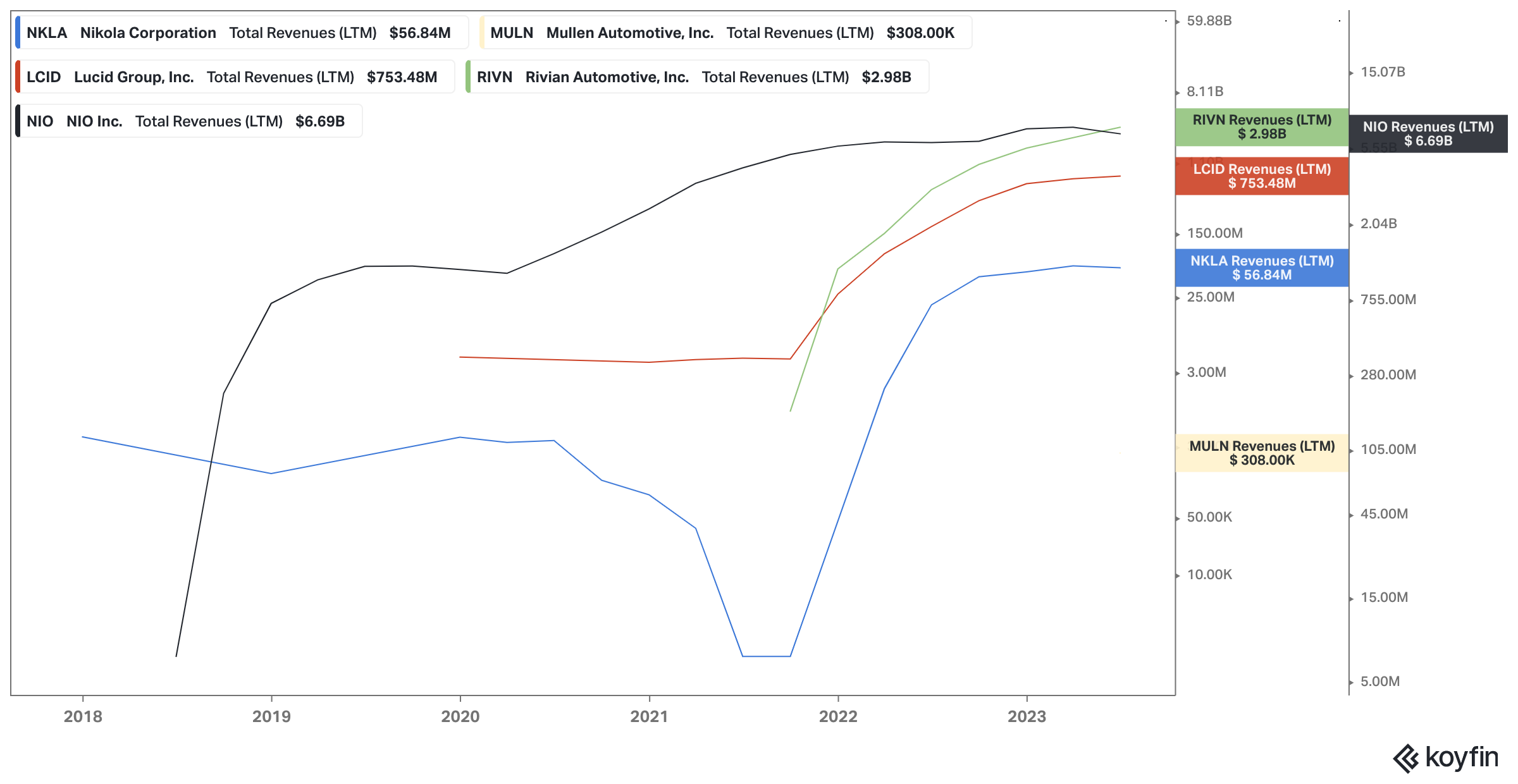

Without revenue, or sales, a company is worthless. If a company doesn’t generate revenue, or isn’t anticipated to generate revenue, then there is absolutely no reason to invest in it, nor is there a basis for it to have a valuation.

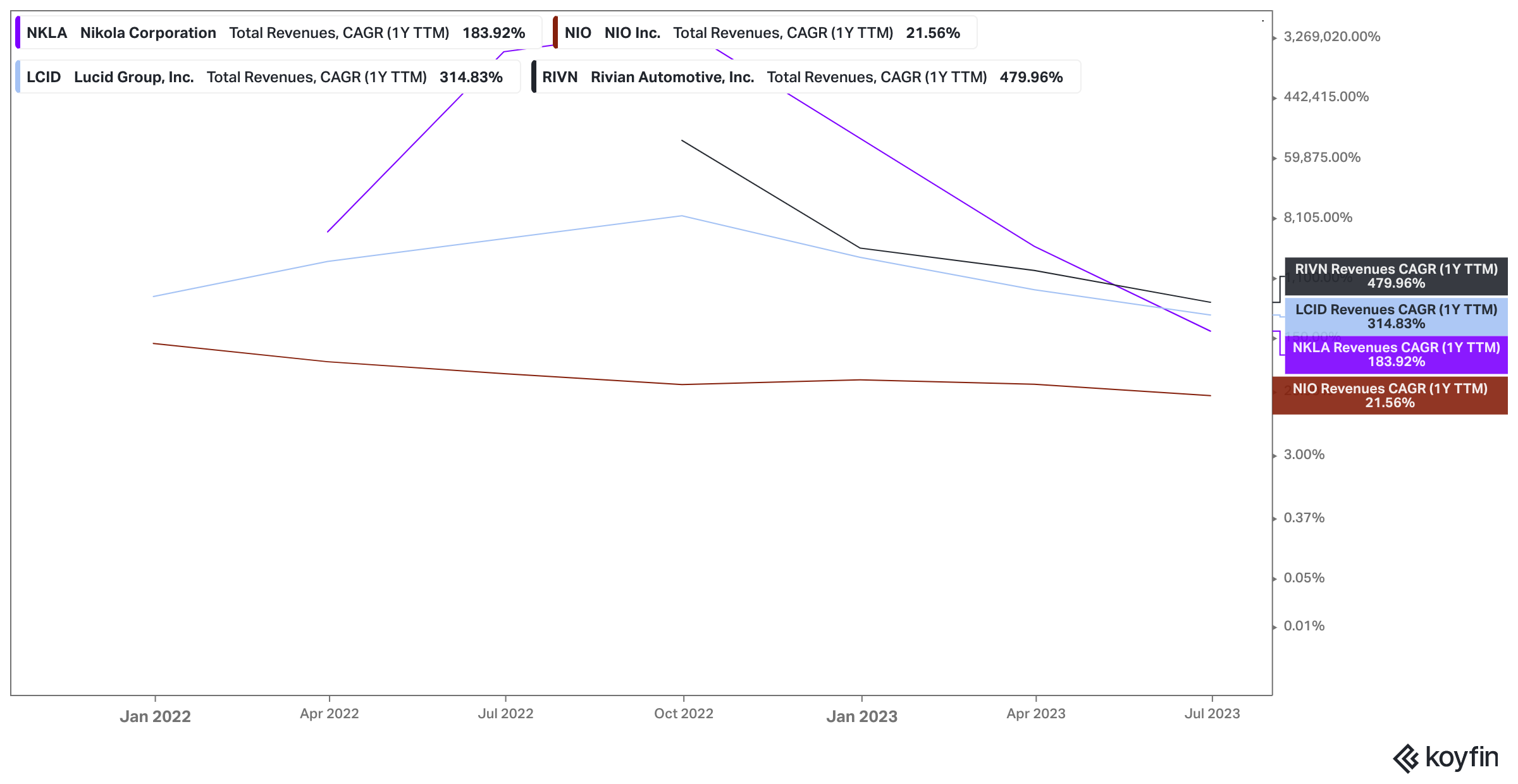

Right off the bat, we can see enormous rates of revenue growth for Rivian, Lucid and Nikola. Needless to say, these rates are unsustainable for the long term, as evidenced by the declining rates of growth in recent quarters, and are indicative of the three companies beginning production in the past few years.

This is especially noticeable with Nio, which has seen its trailing 12 month (TTM) revenue compound annual growth rate (CAGR) fall dramatically compared to 2019, the year after it delivered its first vehicles. A falling CAGR doesn’t mean that a stock will decline; NIO is up by about 35% since 2019 and at one point was up 870%.

Mullen’s revenue CAGR is not presented on the chart because it recently reported revenue of $308,000 compared to $0 quarter over quarter. In addition, this revenue may not yet be in Mullen’s hands as of the second quarter since it also reported $308,000 in accounts receivable.

We can see that Rivian, Lucid, and Nio are the best positioned in terms of both revenue and revenue growth within the group. While Nio’s revenue growth has plateaued in recent quarters on LTM sales of $6.69 billion, Rivian’s growth still increased significantly on sales of $2.98 billion. However, Nio is the clear leader in revenue, which should reward it with a nice valuation cushion.

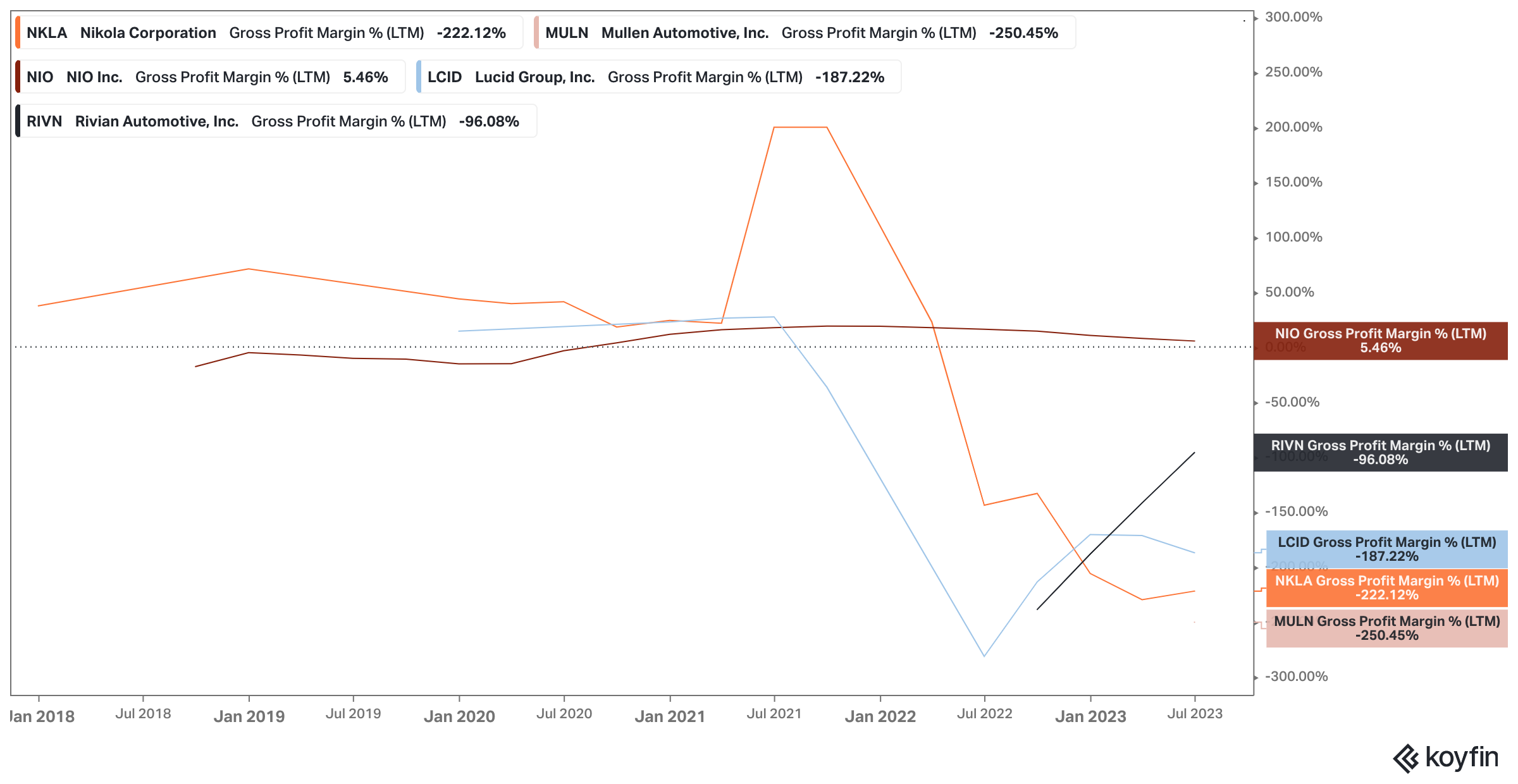

Revenue is an extremely important factor to analyze, although the percentage of revenue actually retained by the company after subtracting out cost of goods sold (COGS) is just as important. That takes us to gross profit margin (GPM).

EV Stocks: Gross Profit Margin

{kind=link}

Car manufacturers have historically experienced low GPMs, which can can be blamed on the sheer amount of components, suppliers, and physical and robotic labor that it takes to manufacture and assemble a vehicle. Accordingly, luxury car manufacturers are likely to have a higher relative GPM due to higher sales prices.

Nio tops off the chart with the only positive LTM GPM of 5.46%, which has fallen every quarter since the high of 19.05% during September 2021. This decline was caused by supply chain challenges, rising battery component costs, and vehicle promotions. During the second quarter, Nio reported a gross margin of just 1%, while its vehicle margin was 6.2%. This means that it retains more money on its vehicle sales than when compared to the rest of its business ventures.

Meanwhile, Rivian displays an impressive trend to the upside, although it still carries a LTM GPM way in the negative. Lucid trails behind with a GPM that has declined in recent quarters. Nikola nears the bottom of the list with a clear downtrend while Mullen finishes in last place.

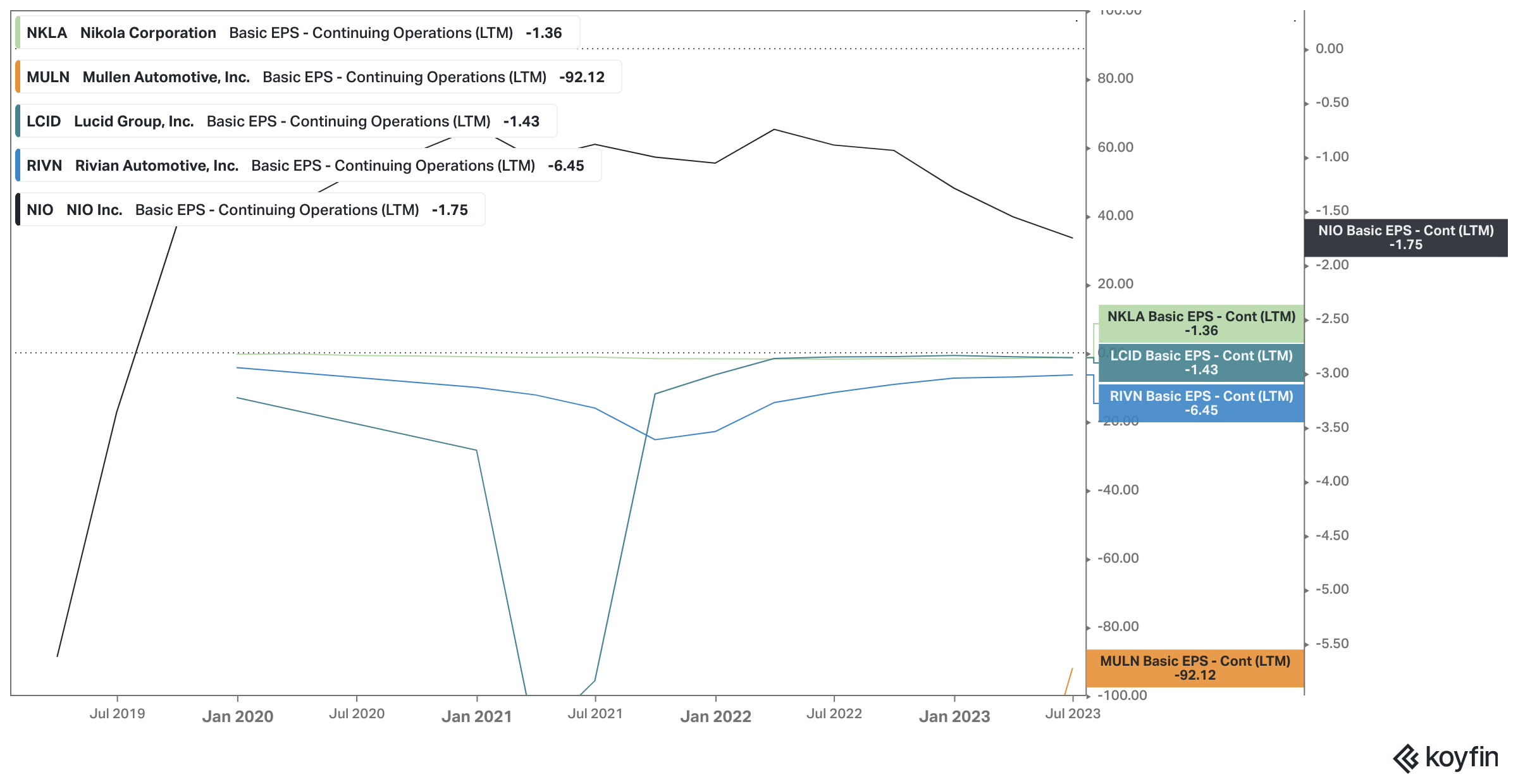

Moving lower on the income statement gets us to the last item: net income or loss. This metric might as well be the bread and butter for any company, as it tells us if a company is profitable after subtracting out COGS, as well as operating expenses and income tax. Dividing net income or loss by the average number of outstanding shares gets us to earnings per share (EPS).

EV Stocks: Earnings Per Share

{kind=link}

All five companies have negative LTM EPS figures, meaning that all five companies were unprofitable over the past year.

Mullen, whose line is restricted by the lower bound of the chart, seems to have the strongest uptrend, although its EPS remains way in the negative. This indicates that shareholders shouldn’t expect profitability anytime soon. Rivian’s EPS has increased every quarter since September 2021, while Nikola leads the pack with Lucid trailing behind by just 7 cents.

Becoming profitable is a key focus point for any company. Why should you invest in a company that will continue to lose money?

We can take a look at analyst EPS estimates on Koyfin to get a better sense of when these five companies will turn a profit on a generally accepted accounting principles (GAAP) basis:

- Nio: 2027 EPS estimate of 77 cents. Nio is also expected to break even in 2026.

- Lucid: 2027 EPS estimate of 2 cents.

- Rivian: 2030 EPS estimate of 43 cents.

- Nikola: Expected to break even in 2026, no further analyst estimates available.

- Mullen: No analyst estimates available. This is likely due to the company’s penny stock status, low market capitalization, and ongoing Nasdaq compliance issues.

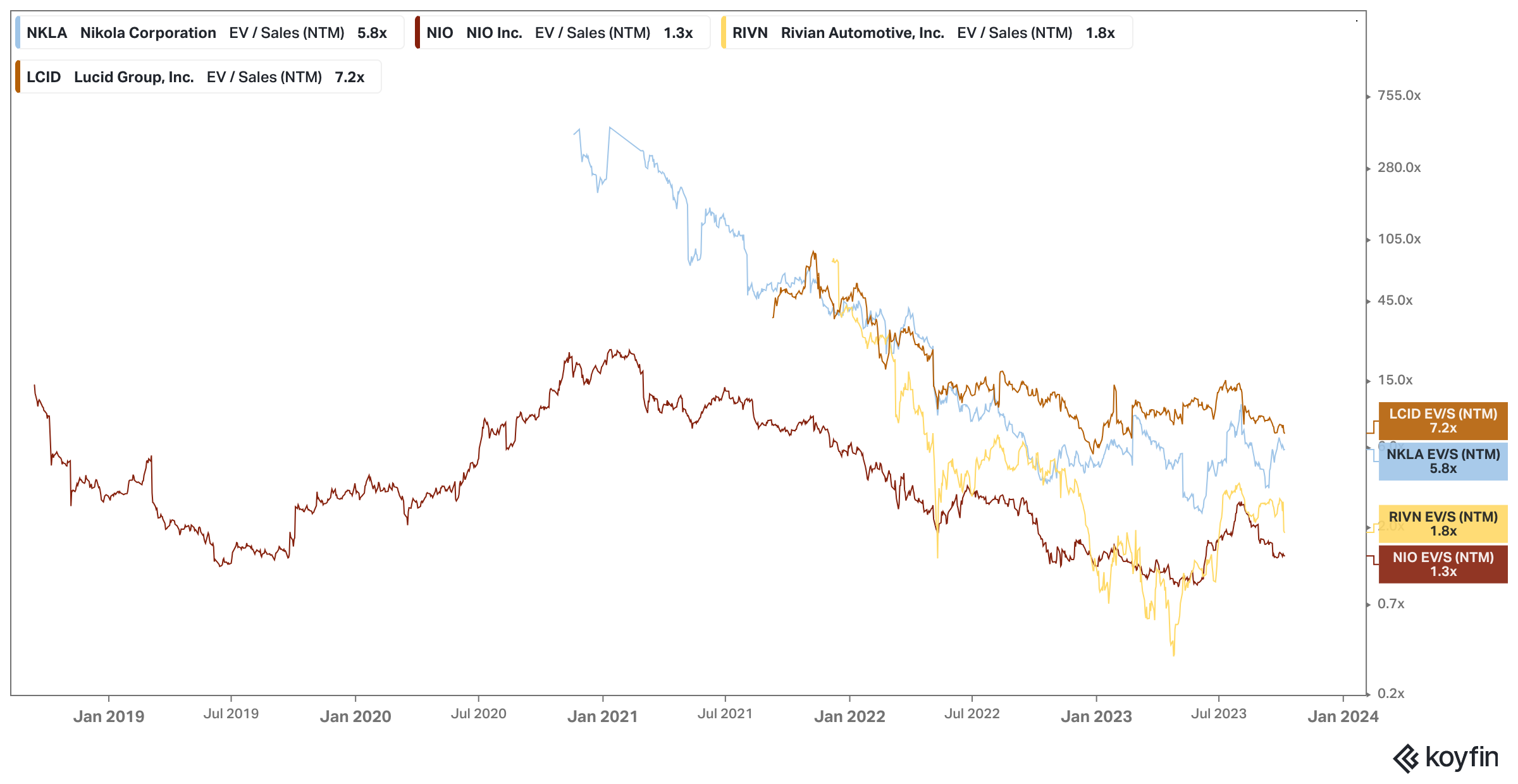

EV Stocks: Valuation Using EV/ Sales

Investing in a good company is a great idea, but investing in a good company that is overvalued is a recipe for disaster.

You can see this theme present in the price of Mullen, which has an all-time return of -99%. Additionally, both Nikola and Rivian have a similar return of -85%. In fact, Nio caries the highest all-time return within the group, which is still a loss of over 10%, while Lucid has a return of about -50%.

To gauge how a company is valued, we can turn to the next 12 months (NTM) enterprise value to sales multiple (EV/S). We use NTM instead of LTM because companies are valued on the basis of their future sales, not their past sales. A higher multiple means that a company is valued higher based on its sales, while a lower multiple signals the opposite. Excluding all other factors, buying a company at a lower multiple is viewed as a better opportunity than buying a company at a higher multiple.

{kind=link}

Lucid is the most richly valued with a NTM EV/S multiple of 7.2x, which has steadily fallen since its public debut. Still, it isn’t alone, as all five companies experienced significant multiple compression from 2021 to late 2022.

2023 has been more generous, as the multiples for the entire group have expanded since the beginning of the year. Mullen does not appear on the chart because no analysts cover its NTM sales estimates.

Valuation shouldn’t be taken into consideration in isolation. Companies with higher revenue, revenue growth, margins, and earnings should be awarded a higher multiple valuation, while companies that have poor financials should trade at a lower valuation. Rivian and Nio are valued at a fair multiple in relation to the group when considering these factors. Nikola’s valuation appears to be bloated, especially given the company’s persistent going concern warnings, poor margins, and slowing revenue growth.

EV Stocks: Comparative Advantages

The quantitative factors covered above are essential to consider when making an investment decision. At the same time, qualitative factors, such as a company’s competitive advantage, are just as crucial to consider.

Competitive advantages can come in many shapes and forms.

For example, Rivian carries a strong competitive advantage due to its close financial relationship with Amazon (NASDAQ:AMZN). The e-commerce giant has placed an order for 100,000 Rivian Electric Delivery Vans (EDVs) by 2030 and is also the largest shareholder of the company. Another advantage that Rivian carries is that the electric truck market has just a few competitors, which provides Rivian with a first-mover advantage and a chance to disrupt the market.

Similarly, Saudi Arabia’s Public Investment Fund (PIF) has invested $5.4 billion into Lucid and is its largest shareholder with a 60.5% ownership stake. The fund has also committed to purchase 50,000 Lucid vehicles over a 10-year period with the option to purchase up to an additional 50,000 vehicles.

Working with a cash-rich, established entity gives theses EV contenders a major head start in the costly production race. PIF’s massive investment has no doubt contributed to the production of Lucid’s proprietary EV powertrain and battery systems, which has attracted attention in the automotive space. In June, Aston Martin announced its entrance into the EV market with a battery electric vehicle (BEV) platform powered by Lucid’s proprietary technology.

Moving across the world gets us to Nio, which continues to lead the group in deliveries. The Chinese EV firm is much more established than any of the other companies and has a unique battery-as-a-service (BaaS) model. With a monthly battery subscription, customers will pay less for the vehicle and also be eligible for Nio’s Power Swap feature. At Power Swap stations, a Nio vehicle can receive a fresh battery in less than 5 minutes. As of July, Nio had installed 1,564 battery swap stations and 7,394 superchargers across China.

Nikola and Mullen’s competitive advantages are difficult to ascertain. Nikola has experienced four truck fires over the past four months and recently announced that it would recall all 209 battery-powered electric trucks that it had distributed. An internal investigation noted that the fires were likely caused by a single supplier component in the battery pack that caused a coolant leak. The consistent fires have caused NKLA stock to plunge lower by about 40% this year.

Mullen doesn’t seem to have any clear competitive advantage in its core vehicles, as they are all sourced from China. Back in 2022, Mullen acquired a 60% controlling interest in Bollinger Motors, which focuses on electric trucks. Unfortunately, Bollinger has yet to sell a single vehicle. At the end of the day, Mullen’s “competitive advantage” may ultimately lie in its loyal investors who swear by the company despite massive net losses. That doesn’t bode well for the company itself, which has shed 99% of its value this year.

EV Stocks: And the Winner Is…

Based on company health, competitive advantages, and valuation, Nio and Rivian are the best investments within the group. Nio can be viewed as a safer investment than Rivian due to its revenue base, low relative valuation, and established charging network, while Rivian is a riskier bet on an early stage company.

Lucid trails behind the two companies due to its inflated valuation and low margins, although the company is more profitable. Nikola commands the highest LTM EPS among the group, but the company’s truck fires, going concern warnings, and revolving management team have severely hurt its reputation. Meanwhile, Mullen remains a company that should be avoided at all costs, given its history of losses, a lackluster management team and shareholder dilution.

At the end of the day, investing in the leader of an industry is always the safest option, and that would be Tesla. If we compare Tesla to the group using the metrics above, it would lead the way in revenue, EPS, and GPM. Tesla’s LTM revenue of $94.03 billion with a GPM of 21.49% blows the rest of the five companies out of the water. These numbers are reflected in its high NTM EV/S multiple of 7.1x, which only trails behind Lucid’s multiple of 7.2x. Although, Tesla has the second-lowest revenue CAGR within the group of 39.99%, it isn’t a cause for concern given its large revenue base.

Investing in these five EV contenders over Tesla could result in higher gains, but it also presents higher risk when taking into account their inferior financial metrics. Tesla has already succeeded in becoming the clear leader in EV industry, while the other companies are still light years away.

On the date of publication, Eddie Pan has a LONG position in AMZN. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.